Understanding Your Colorado Roof Insurance Policy Type

Your policy type determines how much money you'll actually receive after filing a claim. Colorado homeowners typically carry one of two coverage structures: Replacement Cost Value (RCV) or Actual Cash Value (ACV). The difference between them can mean thousands of dollars out of your pocket.

RCV policies pay the full cost to replace your roof with new materials, minus your deductible. If your replacement costs $18,000 and you carry a $2,000 deductible, you receive $16,000. ACV policies, by contrast, factor in depreciation based on your roof's age and condition. That same $18,000 roof might be deemed worth only $9,000 after depreciation is applied to 15-year-old shingles. Subtract your $2,000 deductible, and you're looking at a $7,000 payout — leaving you to cover the $11,000 gap yourself.

Many homeowners don't discover they have ACV coverage until they're already deep into the claims process. Pull your policy documents now and locate the "Dwelling Coverage" section. If it specifies "Actual Cash Value" or includes depreciation language, you're working with limited payout potential. RCV policies often include a two-payment structure called recoverable depreciation, where the insurer issues an initial ACV payment and releases the depreciation amount after you complete repairs and submit proof of payment.

Deductibles and Premium Discounts in Colorado

Wind and hail deductibles in Colorado have climbed significantly over the past five years. Where $1,000 flat deductibles were once standard, many policies now carry percentage-based deductibles of 1-2% of your home's insured value. On a home insured for $500,000, a 2% deductible means you're responsible for the first $10,000 of any claim.

Insurers offset these higher deductibles with premium discounts for Class 4 impact-resistant shingles — typically 15-28% annually. If you're planning a roof replacement anyway, upgrading to impact-rated materials can reduce your premiums enough to recover the added material cost within 5-7 years. Verify your discount eligibility with your carrier before installation, and confirm the contractor documents the upgrade properly on building permits and final invoices.

When to File a Roof Insurance Claim in Colorado

Not every roof issue warrants an insurance claim. Filing for minor damage can raise your premiums without delivering meaningful financial benefit, especially if repair costs fall below your deductible. Colorado's high-deductible environment makes this calculation more important than ever.

File a claim when damage meets or exceeds your deductible amount and stems from a covered peril — typically wind, hail, fire, or falling objects. Storm-related claims generally don't increase your individual rates, though this varies by carrier and your overall claims history. A single hail claim after a major Front Range event usually won't trigger a rate hike. Three claims in five years might.

Timing Windows and Statute of Limitations

Colorado law doesn't impose a specific deadline for filing roof damage claims, but your policy almost certainly does. Most carriers require written notice within one year of the loss date. Some policies tighten this to 180 days or even 60 days. The "loss date" is the date the damage occurred — not the date you discovered it.

This catches homeowners off guard more often than any other policy provision. You might not notice roof damage until months after a hailstorm, when water stains appear on bedroom ceilings or insulation gets soaked. By then, you're racing against a deadline you didn't know existed. If you suspect storm damage occurred, schedule a professional roof inspection immediately. Waiting until visible interior damage appears can push you past your filing window.

Colorado's statute of limitations for breach of insurance contract is two years from the date of loss for first-party claims. If your insurer denies a claim or undervalues damage, you have two years to file suit. This is separate from your policy's filing deadline — missing the policy deadline can void your right to file in the first place.

Documenting Roof Damage Before You File

Insurance adjusters approve or deny claims based on physical evidence. Your ability to photograph damage, preserve the loss scene, and document pre-storm condition determines how smoothly the process goes.

Start with exterior documentation. Walk your property after any significant hail or wind event and photograph damage to vehicles, siding, gutters, fence tops, and AC units. Hail that dents a car hood or cracks vinyl siding almost certainly damaged your roof. These ground-level indicators give adjusters corroborating evidence that supports roof damage claims. Time-stamp your photos — most smartphones embed GPS coordinates and timestamps automatically. If your device doesn't, email the images to yourself immediately to create a verifiable record.

Hire a licensed roofing contractor for a formal inspection before filing. Many Colorado roofing companies offer free roof inspections and hail damage assessments — not as a sales gimmick, but because identifying damage early protects both you and them. Contractors familiar with insurance claim assistance know what adjusters look for: bruised or cracked shingles, compromised granule coverage, damaged flashing seals, dented vents and pipe boots, and compromised valley integrity.

Ask the contractor to mark damaged areas with chalk or flagging before the adjuster arrives. This sounds excessive, but hail bruising on dark shingles can be nearly invisible from ground level. Flagged damage speeds up the inspection and reduces the chance an adjuster misses compromised zones during a 20-minute walkthrough. Request a written damage report with annotated photos showing impact locations, direction of denting, and measurements of affected zones.

Interior Damage Documentation

If water infiltration has already occurred, document every affected area. Photograph ceiling stains, saturated insulation, wall discoloration, and any damaged personal property. Measure stain dimensions and note the date you first observed them. Pull insulation samples from your attic if they're wet — bag them, label them with the date, and store them as evidence.

Do not make permanent repairs before the adjuster inspects. Colorado law allows temporary emergency repairs to prevent further damage — tarping a punctured section or placing buckets under active leaks is fine. Ripping out water-damaged drywall or replacing compromised decking before documentation occurs can void your claim. If you must make emergency repairs to prevent additional loss, photograph every step and save all removed materials.

The Insurance Adjuster Inspection Process

Your insurer will assign an adjuster within 15-30 days of your claim filing under typical circumstances. During peak hail season along the Front Range — generally June through August — major carriers face significant backlogs. Denver metro adjusters during these periods can run 60-90 days behind, especially after widespread storms like the 2023 Highlands Ranch event that generated 40,000+ claims in a single afternoon.

If your insurer hasn't responded within 30 days of your initial claim, push back in writing. Colorado insurance regulations require prompt investigation and reasonable communication. Document every interaction: save emails, log phone calls with dates and representative names, and send follow-up letters via certified mail if response times stretch past 45 days.

What Adjusters Look For

The adjuster will inspect your roof, attic, and any interior damage zones. Most spend 30-60 minutes on-site, measuring damage density (impacts per 100 square feet), evaluating granule loss, checking flashing and penetration seals, and assessing whether damage resulted from the reported storm event or pre-existing wear.

Colorado adjusters use impact testing squares — typically 10×10 grids placed randomly across roof sections. They count verifiable hail strikes within each square and calculate an average. Eight or more impacts per 100 square feet generally meets the threshold for full replacement approval in most policies. Fewer impacts might justify partial repairs or shingle replacement in specific zones.

You or your contractor can be present during this inspection. Having your roofer there isn't mandatory, but it helps — they can point out damage the adjuster might miss and answer technical questions about installation methods or material specifications. Some adjusters prefer homeowners-only inspections. If yours requests this, you can still have your contractor conduct a separate inspection afterward and submit a supplemental damage report if discrepancies exist.

Disputing Insufficient Initial Assessments

Adjusters sometimes underestimate damage scope, particularly on older roofs where hail impacts blend with existing weathering. If the adjuster's preliminary estimate seems low or denies damage your contractor clearly documented, you can request a re-inspection or submit a contractor-prepared supplement.

Most carriers allow homeowners to provide additional evidence within 30-60 days of the initial assessment. Your contractor will prepare a detailed supplement documenting missed damage, supported by photos and measurements. Adjusters frequently approve supplemental claims when the evidence is clear and well-documented — this isn't adversarial, it's part of the normal process in Colorado's high-claim environment.

Choosing Your Roofing Contractor

You are not required to use your insurance company's recommended contractors. This is your legal right in Colorado, and exercising it protects your interests. Insurance-preferred vendors may offer convenient direct billing, but they work within strict pricing guidelines that can limit material choices, installation methods, and warranty coverage.

Instead, vet contractors the way you'd choose any major home service provider. Verify local licensing — while Colorado doesn't require state-level roofing licenses, Denver, Colorado Springs, Aurora, Boulder, Fort Collins, and Lakewood all maintain municipal contractor registries at https://www.colorado.gov/dora. Confirm workers' compensation coverage (required for all contractors with employees) and general liability insurance (required by most municipalities and HOAs).

Don't collect three impersonal bids and choose the cheapest. Think of this process like getting multiple medical opinions — you're looking for a contractor you know, like, and trust who understands Colorado's insurance claims process. A quality contractor will review your adjuster's estimate line by line, identify undocumented damage, and handle supplement negotiations directly with your insurer.

Storm Chasers vs. Local Contractors

Major hail events bring an influx of out-of-state contractors who canvass neighborhoods immediately after storms. These "storm chasers" aren't necessarily dishonest, but they operate under a business model that prioritizes volume over relationships. They'll be gone within 6-12 months, leaving you with no recourse if workmanship issues appear or warranty claims arise.

Local contractors maintain permanent offices, employ year-round crews, and stake their reputations on long-term customer relationships. They pull permits properly, understand municipal code requirements, and show up for warranty work three years later when a valley seal starts weeping. Verify how long a contractor has operated in Colorado and whether they maintain a physical office you can visit.

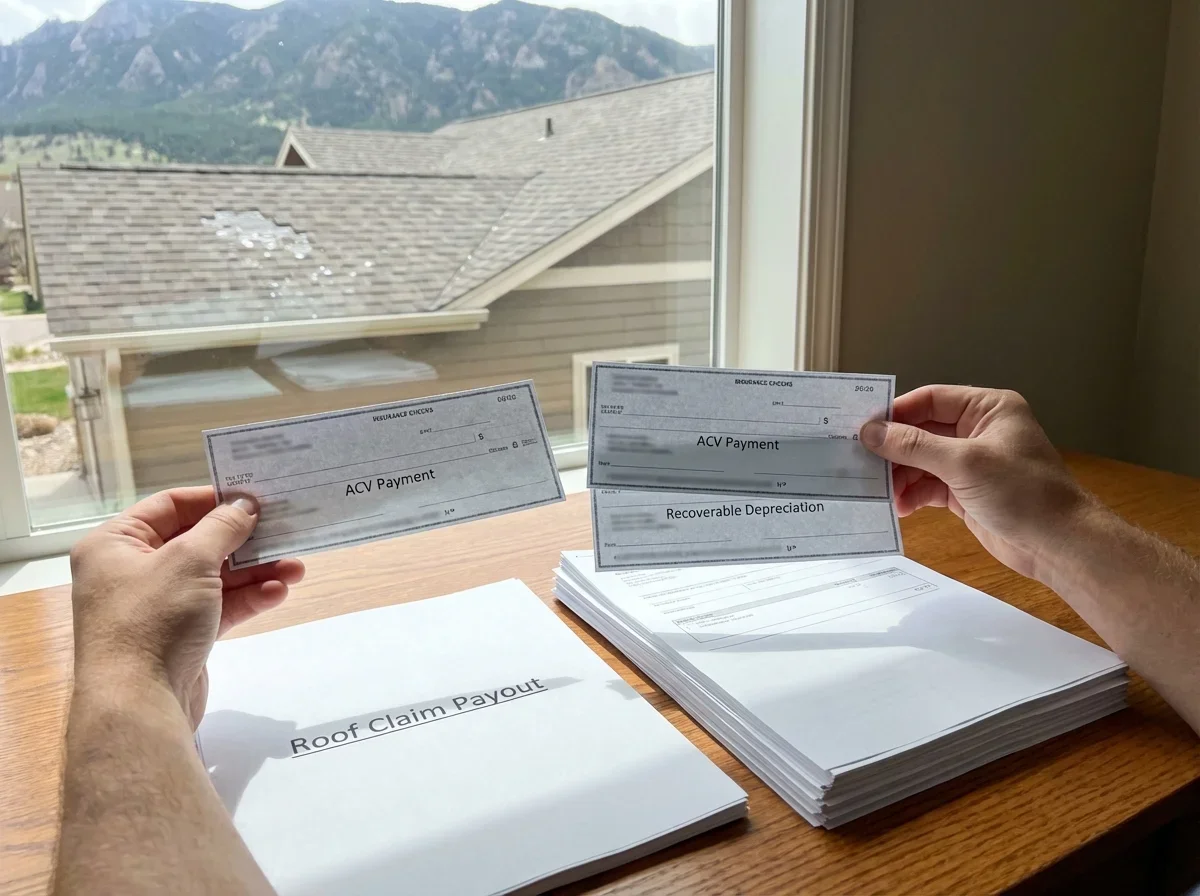

Understanding Actual Cash Value vs. Replacement Cost Payouts

If you carry RCV coverage, your insurer will typically issue two checks: an initial ACV payment that covers depreciated value minus your deductible, and a recoverable depreciation payment released after you complete repairs.

Here's how this works in practice. Your 2010 architectural shingle roof needs full replacement after a hailstorm. The RCV is $22,000. Your insurance company calculates $8,000 in depreciation based on the roof's 16-year age and deducts your $2,000 deductible. You receive an initial check for $12,000 ($22,000 - $8,000 - $2,000).

After your contractor completes the work and you submit final invoices and proof of payment, the insurer releases the $8,000 recoverable depreciation. You now have the full $20,000 RCV amount minus your deductible. If you don't complete repairs, you forfeit the recoverable depreciation — it stays with the insurance company.

Using Insurance Funds Properly

Colorado law prohibits misusing insurance settlement funds. If your carrier issues a check for roof replacement and you use that money for a kitchen remodel instead, you've committed insurance fraud — a class 5 felony that carries penalties up to three years imprisonment and $100,000 in fines.

This applies even when you own your home outright. If you carry a mortgage, your lender's name will appear on the settlement check as a co-payee. You'll need to obtain their signature before depositing funds, and they may require proof of completed work before releasing their interest. This protects the lender's collateral — your home — from unrepaired damage that could compromise property value.

When to Hire a Public Adjuster

Public adjusters are licensed professionals who represent policyholders in insurance claims negotiations. They review damage, prepare detailed loss estimates, and negotiate directly with your insurance company's adjuster on your behalf. Colorado licenses public adjusters through the Division of Insurance — verify credentials at https://www.colorado.gov/dora before hiring.

Public adjusters make sense in specific scenarios: when your claim is denied despite clear damage, when your carrier's estimate is significantly lower than your contractor's scope of work, or when damage is complex enough that you lack confidence in your ability to document it properly. They typically charge 10-15% of your final settlement amount, paid only if they secure compensation.

For straightforward hail damage on a standard residential roof, you probably don't need a public adjuster. A quality local contractor who understands the claims process can handle supplement preparation and adjuster negotiations as part of their service. Public adjusters add value when claims involve significant disputes, multiple damage types (roof + siding + gutters + interior), or carriers with reputations for aggressive claim resistance.

Appealing Denied Claims

If your insurer denies your claim, they must provide written explanation referencing specific policy language and reasons for denial. Vague rejection letters violate Colorado claim-handling regulations. You have the right to dispute this decision.

File your written dispute within 30-60 days of receiving the denial letter — your policy specifies the exact window. Include all supporting documentation: contractor damage reports, photos with timestamps, weather event verification from National Weather Service records, and any technical evidence that contradicts the denial reasoning.

Appeals in Colorado typically resolve within 2-8 weeks. If the internal appeal fails, you can file a complaint with the Colorado Division of Insurance or pursue civil litigation. Most disputes settle during the internal appeal process when homeowners provide thorough documentation — insurers prefer avoiding regulatory scrutiny and legal costs.

Permit Requirements and Code Compliance

Most Colorado municipalities require permits for roof replacement work. Denver, Colorado Springs, and Boulder all mandate permits for tear-offs and full replacements, though some jurisdictions allow permit-exempt repairs under specific dollar thresholds. Your contractor should handle permit applications — if they suggest skipping this step to save money, find a different contractor.

Permitted work ensures code compliance with International Building Code (IBC) and International Residential Code (IRC) requirements as adopted by your municipality. Inspectors verify proper flashing installation, adequate ventilation, correct fastener patterns, and appropriate material specifications. Unpermitted work can void manufacturer warranties, complicate future insurance claims, and create disclosure issues when you sell your home.

Colorado's building codes include specific provisions for high-wind zones and snow load requirements. Front Range communities incorporate 90+ mph wind ratings in their code amendments. Mountain jurisdictions above 8,000 feet mandate enhanced snow load calculations — your contractor needs to understand these regional variations. Insurance companies sometimes deny claims on unpermitted work, arguing that code violations contributed to failure.

Impact-Resistant Shingles and Insurance Discounts

Class 4 impact-resistant shingles have become the de facto standard for Colorado roof replacements. These shingles are UL 2218 rated to withstand impacts from 2-inch hail — roughly golf ball sized — without compromising their waterproofing integrity.

Installing Class 4 shingles qualifies you for insurance premium discounts ranging from 15-28% annually, depending on your carrier. On a $2,500 annual premium, that's $375-$700 in savings every year. The material upgrade typically adds $1,500-$3,000 to replacement costs, meaning you recover the investment through premium savings in 4-6 years.

Verify discount eligibility before installation. Most carriers require proof of UL 2218 Class 4 certification — your contractor should provide product specification sheets and ensure the classification appears on building permits and final invoices. Some insurers require photos of bundles showing UL labels. Missing this documentation can void your discount eligibility even when the correct materials were installed.

You can learn more about specific product options and performance characteristics in our Class 4 impact-resistant shingles guide.

Handling Supplemental Claims

Initial adjuster estimates frequently undercount damage scope. As contractors tear off old materials and expose the roof deck, they often discover issues invisible during the surface inspection: compromised plywood decking, damaged valley metal, deteriorated flashing, or inadequate ventilation that contributed to failure.

This is normal. Colorado roofing contractors submit supplemental claims on roughly 60% of insurance jobs. Your contractor documents newly discovered damage with photos and measurements, prepares a line-item supplement, and submits it to your adjuster for review. Most supplements are approved within 7-14 days when documentation is clear.

You don't need to do anything during this process beyond signing authorization forms allowing your contractor to communicate with your insurer. Contractors experienced in storm damage repair handle supplement negotiations as a standard part of project management. If the adjuster denies supplement items, your contractor can request a re-inspection or provide additional technical evidence supporting the claim.

What Contractors Can and Cannot Do

Colorado law prohibits contractors from offering to cover your insurance deductible. This is considered rebating, and it's illegal under state statutes designed to prevent insurance fraud. Contractors who advertise "we pay your deductible" or offer equivalent-value upgrades to offset deductible costs are violating the law — and working with them can jeopardize your claim.

You must pay your full deductible. Contractors can offer payment plans or financing options, but the deductible amount itself cannot be waived, discounted, or absorbed into project costs. If a contractor suggests otherwise, that's a red flag indicating they're either uninformed about Colorado regulations or deliberately skirting them.

Contractors can review your insurance estimate, identify undocumented damage, prepare supplements, and communicate directly with adjusters when you authorize them to do so. They cannot negotiate your deductible, pressure you to file claims for marginal damage, or promise specific settlement amounts — those decisions rest with your insurance company based on policy terms and damage evidence.

Seasonal Considerations and Repair Timelines

Colorado's roofing season runs April through October along the Front Range, with mountain communities restricted to May through September due to temperature limitations on shingle adhesive activation. This compressed timeline creates scheduling challenges after major hail events.

A significant June hailstorm can generate 18-24 month repair backlogs as thousands of homeowners compete for limited contractor availability. If you file a claim in July after a major event, you might not get on a contractor's schedule until the following spring. Most insurance policies don't require you to complete repairs within a specific timeframe, but leaving damaged roofs exposed through winter invites secondary damage that may not be covered.

Communicate timeline expectations clearly with your insurer. If contractor backlogs will delay repairs past typical completion windows, get written confirmation that your coverage remains active and that winter weather damage won't be excluded from your claim. Some carriers require annual renewal of open claims — missing these renewal deadlines can close your claim prematurely.

Working with Your Mortgage Lender

If you carry a mortgage, your lender holds a financial interest in your property and must co-endorse insurance settlement checks. The lender's name appears on the check alongside yours — you cannot deposit it without their signature.

This isn't your insurance company being difficult. It's standard mortgage security protocol protecting the lender's collateral. Contact your lender immediately after receiving settlement funds. Most have specific claims departments that handle insurance disbursements. You'll typically need to provide:

- A copy of the insurance settlement check

- Your contractor's detailed scope of work and estimate

- Building permit documentation

- Proof of contractor licensing and insurance

The lender may release funds in stages as work progresses, holding final payment until you submit completion certificates and lien waivers. This protects both you and the lender from contractor default or incomplete work. Factor these timeline requirements into your project planning — lender approval can add 2-4 weeks to your schedule.

Hail Damage vs. Normal Wear and Tear

Insurance covers sudden, accidental damage from covered perils. It does not cover normal deterioration, deferred maintenance, or age-related failure. Colorado adjusters scrutinize roof age carefully because UV exposure at 5,280 feet degrades materials 25-30% faster than sea-level environments.

A 20-year-old roof with granule loss and cracked shingles probably won't be covered even if a hailstorm occurred. Adjusters will argue the roof failed due to age, not storm impact. A 10-year-old roof with similar damage after a documented hail event has a much stronger claim.

This is why documentation matters so much. If you have photos showing your roof in good condition before the storm, you establish that damage occurred suddenly rather than gradually. Annual roof maintenance programs that include periodic inspections create a documented condition history — useful evidence if you need to prove storm damage later.

Colorado-Specific Claims Considerations

Colorado's expansive clay soil along the Front Range causes foundation movement that shifts rooflines and stresses flashing seals. This creates a gray area in claims where storm damage and soil movement interact. An adjuster might argue that a leaking valley resulted from foundation settlement rather than hail impact.

Counter this by documenting the timeline. If valley leaks appeared within weeks of a hailstorm, that suggests storm causation. If your home has experienced ongoing foundation issues for years, the insurer's argument gains credibility. Foundation movement damage typically falls under earth movement exclusions in standard homeowner policies — storm damage does not.

Mountain communities face unique challenges with snow load and ice dam damage. Ice dams form from heat loss melting roof snow, which refreezes at eaves and forces water under shingles. This process-based damage may not be covered under standard policies even though it stems from weather. Understanding these distinctions helps you frame claims properly and set realistic expectations about coverage.

Frequently Asked Questions

Get Colorado-specific pricing based on material, region, and roof size.